The difference between rent-to-own and traditional bank car finance is broader than the monthly instalment. A proper comparison considers the route to ownership, the total cost over the term, the treatment of insurance and maintenance, the approval criteria, default consequences and the contractual rights of each party.

Core differences between the two models

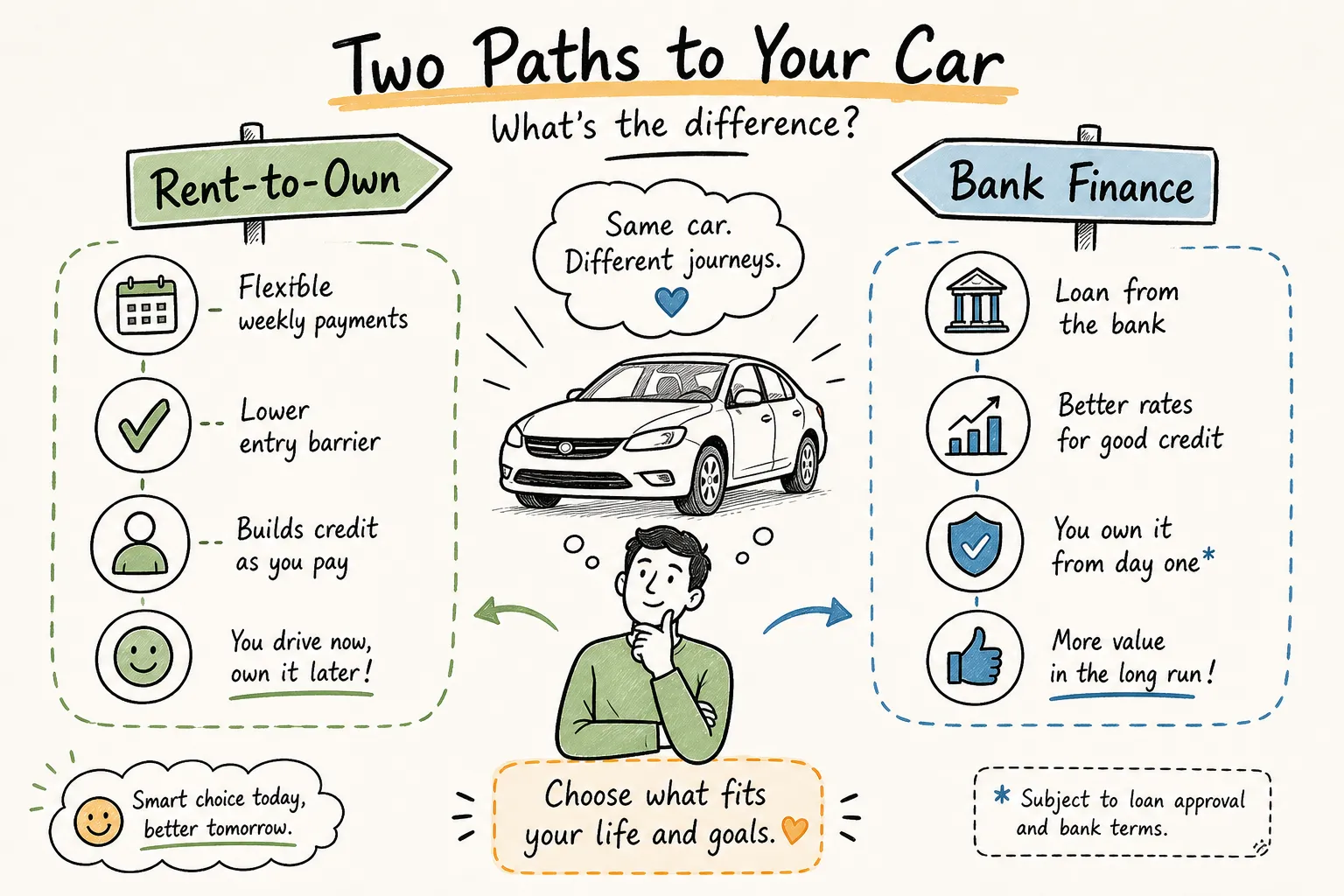

a. Ownership path and timing

Rent-to-own generally gives the customer use of a vehicle during the contract term, with ownership transferring only after the customer satisfies the contractual conditions and any agreed end-of-term requirements. Title usually remains with the provider until those conditions are met.

Traditional bank finance is usually structured as an instalment-sale or hire-purchase credit agreement. The customer takes delivery of the vehicle and repays the financed amount over time. Title is released once the debt is fully settled and all contractual conditions are met.

b. Monthly instalment versus total cost

A bank-finance instalment may appear lower because the customer often pays separately for insurance, licensing, tracking, servicing, tyres and roadside support. A rent-to-own instalment may include selected vehicle-use essentials in one payment, depending on the approved package. The only reliable comparison is the full cost across the same term and vehicle assumptions.

c. Who each option may suit

Bank finance may suit applicants with established credit profiles who want the lowest available borrowing cost and are comfortable managing vehicle-related costs separately. Rent-to-own may suit applicants who need predictable monthly budgeting, value a bundled structure and have stable income but a thin or imperfect credit record. The suitable route depends on affordability, risk tolerance, contract terms and total cost.

Eligibility and approval considerations

a. Traditional vehicle finance

Banks generally assess credit history, affordability, identity documents, bank statements, proof of residence, employment information and insurance arrangements before releasing a vehicle. Applicants with strong credit profiles may receive better pricing. Applicants with weak or thin credit profiles may face additional conditions, adjusted pricing or a decline.

b. Rent-to-own vehicle access

Rent-to-own providers may assess applications by placing greater emphasis on verified income and affordability. However, approval should still include identity verification, fraud screening, compliance checks, contract suitability and internal risk assessment. Customers should not assume that a rent-to-own product avoids all checks or all reporting obligations.

VEN Mobility’s position

VEN Mobility considers proof of income and affordability as important parts of the assessment. Credit history is not the sole determinant. Approval remains subject to internal risk criteria, compliance requirements, document validation and the formal contract terms presented to the applicant.

Cost comparison framework

Applicants should compare written quotes using the same vehicle, term and usage assumptions. The questions to ask differ by product:

| Cost item | Bank finance | Rent-to-own |

|---|---|---|

| Deposit or upfront amount | What deposit, initiation fee or upfront charge is payable? | What deposit or onboarding amount is payable and when? |

| Monthly amount | What is the financed instalment and what costs sit outside it? | What is included in the monthly payment and what is excluded? |

| Insurance | Is comprehensive insurance compulsory and separately arranged? | Is insurance included, and what excesses or exclusions apply? |

| Maintenance and tyres | Which services, tyres and repairs must the customer fund separately? | Which maintenance items are included and which remain the customer’s responsibility? |

| Licensing and tracking | Are licensing, tracking and renewals separate costs? | Are these included in the package or billed separately? |

| End-of-term amount | Is there a balloon, residual or settlement amount? | Is there a buyout, handover amount or ownership-transfer condition? |

| Early exit | What settlement rules, notice periods and penalties apply? | What early termination fees, return rules and condition charges apply? |

| Default consequence | What enforcement steps apply under the credit agreement? | What recovery, arrears and return provisions apply under the rental contract? |

Contracts, risks and legal protections

a. Credit agreement versus rental structure

Instalment-sale vehicle finance is generally regulated under the National Credit Act. Rent-to-own arrangements may be structured differently, and the applicable rights and duties depend on the legal form of the contract. Customers should read the agreement carefully and obtain professional advice where the structure, fees or ownership path is unclear.

b. Repossession, recovery and credit reporting

With bank finance, arrears may lead to credit-agreement enforcement, notices, legal process and possible repossession. With rent-to-own, missed payments may lead to vehicle recovery under the rental terms. Credit-bureau reporting can differ across products and providers. Customers should ask for the reporting position in writing before signing.

c. Early exit, mileage and vehicle condition

Both models can carry costs if the customer exits early. Rent-to-own agreements may also include mileage, use, servicing and vehicle-condition requirements. Customers should document vehicle condition at handover, keep service records and understand excess charges before signing.

What a transparent bundled plan should disclose

A transparent bundled plan should disclose the monthly amount, included items, excluded items, deposit, term, insurance responsibilities, maintenance responsibilities, mileage rules, early-exit costs, arrears process, handover process and ownership-transfer conditions. Customers should not rely on verbal statements where the written contract says something different.

For VEN Mobility, the customer should review the formal quote and contract to confirm the approved package, included vehicle-use essentials, customer responsibilities and end-of-term conditions. Any online estimate should be treated as indicative until the formal offer is issued.

When rent-to-own may make commercial sense

Rent-to-own may be suitable where the customer values predictable monthly budgeting, needs vehicle access despite a thin credit file, or prefers selected vehicle-use essentials to be dealt with through one package. Bank finance may still be more suitable for applicants with strong credit profiles who qualify for competitive pricing and can manage separate running costs without cash-flow pressure.

Ten questions to ask before signing

- What is the deposit or upfront amount, and when is it payable?

- What is the full contract term and can it be shortened or extended?

- What is the total cost over the term, including fees and any end-of-term amount?

- What exactly is included in the monthly payment?

- What costs remain the customer’s responsibility?

- Are there mileage limits, use restrictions or excess charges?

- What happens if the customer misses a payment?

- How does early termination work and what does it cost?

- How is payment history reported, if at all?

- When and how does ownership transfer?

How to compare quotes fairly

Use the same vehicle, term, deposit, annual kilometres and ownership objective. Then add every compulsory cost, including insurance, maintenance, tyres, licensing, tracking, fees, balloon amounts, buyout amounts and penalties. The correct comparison is not the lowest monthly figure. It is the total written cost of access or ownership under comparable assumptions.

When to walk away

Walk away from vague fees, unclear return conditions, undocumented add-ons, missing service-plan clarity, unexplained recovery rights or a provider that cannot disclose the total cost structure in writing. A customer should not sign unless the route to possession, use, payment, default and ownership is clear.