A stable monthly income can support a vehicle-finance application, but income alone does not usually determine the outcome. South African lenders typically assess affordability, identity documentation, residence information, bank-statement behaviour, existing financial commitments and credit-bureau information before approving a vehicle-finance product.

The practical question is therefore not whether proof of income matters. The better question is which finance route fits the applicant's profile. Traditional bank finance normally requires a broader credit assessment. Alternative vehicle-access models may place greater weight on current income and affordability, subject to identity verification, fraud screening, compliance checks and internal risk criteria.

Can I get a car on finance with only proof of income?

Proof of income can open the conversation, but it should not be treated as a complete application. Mainstream banks usually require an affordability assessment and credit review before they approve vehicle finance. Rent-to-own and other alternative mobility models may assess applications differently, but approval remains subject to documented affordability, contract terms and responsible customer onboarding.

What banks usually require beyond a payslip

Typical document checklist

Most mainstream vehicle-finance applications require more than a payslip. A typical application may include identity documents, a valid driver’s licence, proof of residence, recent payslips or bank statements, employment information, affordability declarations and proof of comprehensive insurance where applicable. Requirements differ by lender and may change, so applicants should confirm the current criteria directly before applying.

Why the credit assessment matters

A payslip shows what an applicant earns. It does not, on its own, show spending patterns, existing commitments, repayment behaviour or available monthly capacity. Credit-bureau information and bank-statement conduct help lenders assess whether a proposed instalment is sustainable. A thin or inactive credit file can create uncertainty even where income appears stable.

Which income documents may support an application

a. Bank statements as proof of consistent income

Bank statements are commonly used to evidence recurring income, particularly for self-employed applicants, commission earners, contract workers and informal traders who receive payments through a bank account. Lenders generally look for consistency, traceability and affordability rather than a single deposit in isolation.

b. Other supporting documents

Depending on the applicant’s employment profile, supporting evidence may include payslips, employment contracts, tax certificates, client contracts, invoices and bank statements. Documents that do not show recurring, verifiable income are usually insufficient on their own. Applicants should avoid submitting incomplete files because unnecessary applications may create avoidable credit enquiries.

How your credit profile can affect the deal

Applicants with established repayment histories may have access to wider lender choice and better pricing. Applicants with thin, inactive or impaired credit records may face additional conditions, adjusted pricing, higher deposits, shorter terms or a decline. The exact outcome depends on the lender, the vehicle, affordability, contract structure and prevailing market conditions.

For this reason, applicants should compare the full cost of access rather than focusing only on the advertised monthly instalment. Insurance, maintenance, licensing, tracking, roadside support, deposits, fees and end-of-term amounts can materially change the real affordability position.

Who traditional vehicle finance may exclude

a. Income earners with thin credit files

First-time buyers, young professionals, gig workers, domestic workers, informal traders and newly formalised employees may earn consistently but have limited formal borrowing history. This can make a bank application difficult even where the applicant manages personal expenses responsibly.

b. Applicants rebuilding after financial difficulty

Some applicants have historic credit issues but now receive stable income and manage their finances more effectively. Conventional credit systems may still treat this history as a risk factor. Alternative vehicle-access models may provide a more suitable assessment route, provided affordability and compliance checks are satisfied.

VEN Mobility: vehicle access assessed through affordability

VEN Mobility offers a rent-to-own vehicle-access model for applicants whose income is stable but whose profile may not fit conventional bank finance. The assessment considers proof of income, affordability, identity verification, fraud screening, compliance checks and VEN Mobility’s internal risk criteria. Credit history is not the sole determinant, but approval is never automatic.

Applicants may submit payslips, bank statements or other acceptable proof of recurring income, subject to validation. Any indicative quote should be read together with the formal offer and contract documents before the applicant commits.

What the monthly payment may cover

A single monthly payment includes selected vehicle-use essentials, depending on the approved package, vehicle, term and customer profile. The contract should confirm exactly what is included, what is excluded, what excesses or customer responsibilities apply, and what happens at the end of the term.

Practical steps before applying

- Prepare complete and current identity, driver’s licence, address and income documents before applying.

- Use bank statements to evidence recurring income where a standard payslip does not reflect the full income position.

- Check affordability after rent, transport, food, insurance, debt commitments and other fixed costs.

- Ask every provider to disclose the total cost of access or ownership, not only the monthly instalment.

- Read the contract terms on deposits, term, maintenance responsibilities, insurance, early exit, vehicle recovery, handover and ownership transfer.

Frequently asked questions

Can I get a car with only proof of income?

Proof of income may support an application, but most providers will still assess affordability, identity, compliance and contract suitability. Mainstream banks usually also conduct a credit assessment.

Do banks accept bank statements instead of payslips?

Some lenders may accept bank statements as part of the income assessment, particularly for non-salaried applicants. Requirements differ by lender and should be verified directly.

What happens if I have income but no credit record?

A thin credit file may limit access to mainstream bank finance. Alternative mobility models may place greater emphasis on current affordability, but approval remains subject to checks and contract terms.

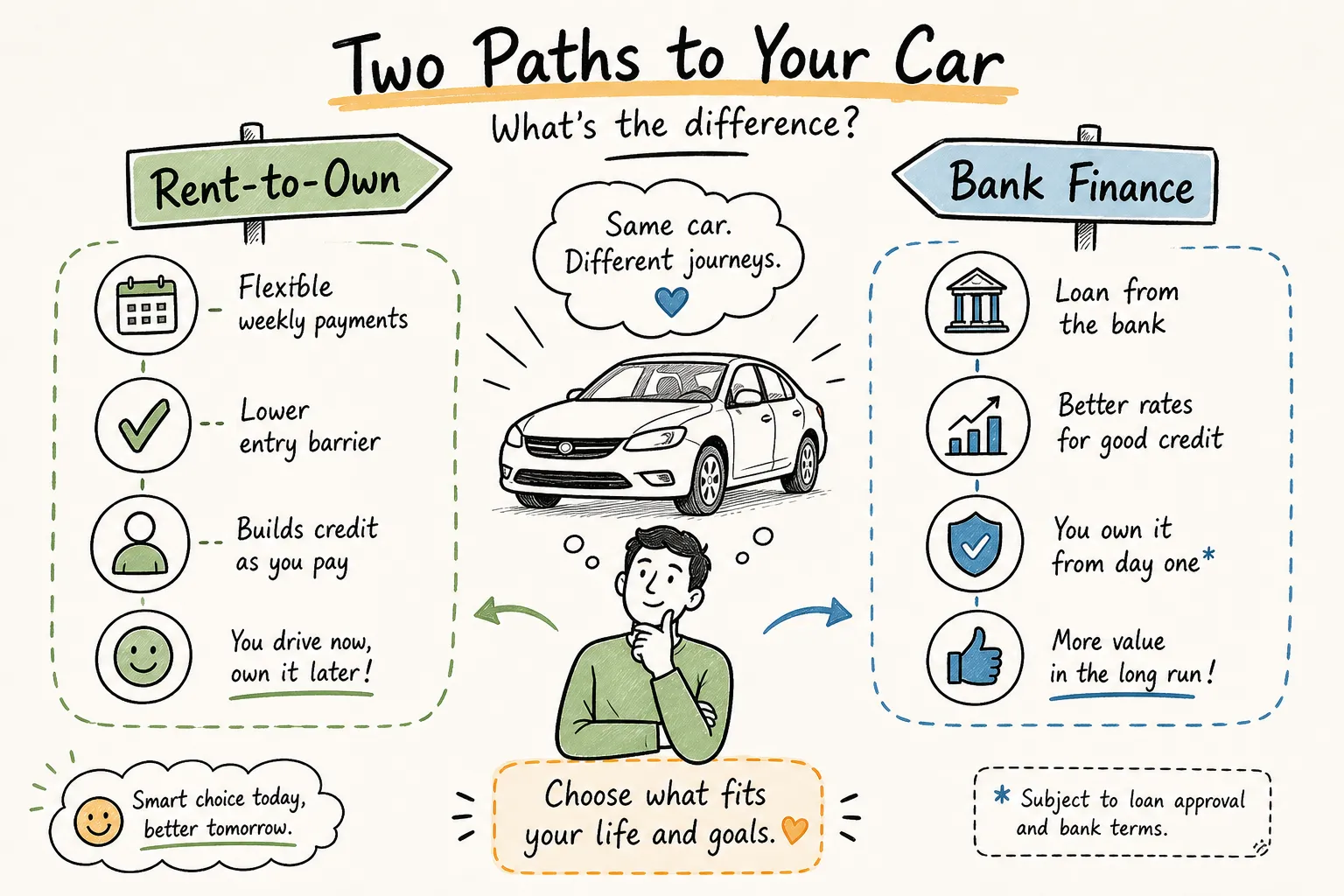

Is rent-to-own the same as bank finance?

No. Bank finance is typically a credit agreement, while rent-to-own is structured differently. The exact rights, duties and ownership path depend on the signed contract and applicable law.

The bottom line

Proof of income is important, but it is not always sufficient for traditional bank vehicle finance. Applicants should choose the route that fits their income pattern, credit profile, affordability and risk tolerance. A transparent rent-to-own model may be suitable where the applicant needs predictable costs and an assessment that gives meaningful weight to current affordability. The decision should be based on written terms, full cost disclosure and a careful affordability review.